Richard Oldfield - part I

Richard Oldfield of Oldfield Partners is a seasoned Value investor whose distinguished career in financial markets spans five decades.

Beginning in 1977, he joined Warburgs' international investment department, a move that defined his professional life. Over the years, Oldfield has held significant leadership roles. These include heading of the US equity team at Mercury Asset Management and the founding of Oldfield Partners, a Value equity manager.

In addition, he has extensive experience both managing and advising on the wealth of family offices. Highly regarded for his governance expertise, Oldfield has served on numerous investment committees. Notably, he chaired the Oxford University investment committee, successfully spearheading the creation of a central endowment management company for the university. He is also the author of the acclaimed investment book Simple but Not Easy, which champions the fundamental principles of equity investing.

In the first part of our interview, we explore Oldfield’s childhood passions and his formative studies at Oxford. We discuss the mentors who shaped his philosophy, the mass psychology behind historic market crashes, the flaws in macroeconomic theories and the critical importance of avoiding dogmatism on investment committees.

JS: What were you interested in when you were very young and then a bit later in your teenage years?

RO: At 6 and 7 I was interested in being a policeman and I received policeman outfits two Christmases running. Those were the days of Dixon of Dock Green and Z Cars and when the police were an institution that was respected. Today, like a whole lot of other institutions they are not respected. At 10, I was into magic and I got magic sets for Christmas. I was very keen on producing little performances for my very bored family who sat in a polite line watching me do these little tricks. And at 20 I was interested in reading and history. My father was a stockbroker but that had little influence because he didn't really enjoy it very much and he certainly never influenced me positively in favour of stock broking.

However, in the 1960s, one of his partners was Gubby Allen who was manager of the English cricket team that went to Australia who'd been part of the bodyline team in the 1920s with Harold Larwood and Douglas Jardine. Whilst Gubby Allen was in Australia, he went to see various gold mines. Harmony was one of them, Hampton was another. And he came back with these tips and information. I don't know if it was inside information but it was certainly information which was very strong and so I suppose I my father did influence me a little bit by telling me about these companies.

By the age of 15, I had developed an interest in shares and I used very nerdishly to go through the Telegraph share page and look at share prices and I was always interested in shares which were priced very low. I didn't know this was a category of investing called “penny share investing” and I certainly didn't know anything about Value investing but I was instinctively drawn to things that were cheap in a curmudgeonly way.

My first investment was in a share with a share price was 6p. It was the rump that had survived the secondary banking crisis in the early 1970s of Slater Walker and it was the insurance subsidiary which was priced at 6p and I remember thinking that 6p could easily go to 18p and the worst thing that could happen is that the 6p is that it becomes nothing and that there was, and I wouldn't have used this word at the time, an asymmetric risk. And that did work out well because, although I didn’t know it at the time, it was a Value investment as it had been besmirched by its association with Slater Walker. But it was a perfectly proper company with a proper business and the change of name symbolised a change of direction and a new era and it did turn out well.

JS: What sort of career did you think your degree Oxford would project you into and what do you remember about your choices? Was there a graduate milk round?

RO: There was and I was interested in investment. I was interested in joining a merchant bank and I applied to Warburgs and to Rothschilds. Warburgs took me and I set off on the two-year graduate program but within about six weeks I found myself in the international investment department from where I should have been moved on but they were short of people and they asked if I would stay and that was couldn't have been better was exactly what I wanted. I really stayed in the international investment department for the next 50 years.

JS: At Oxford, was there a module of study, or an event that you studied, whose influence has lasted to this day?

RO: British foreign policy before the second World War was my specialist subject and it is still is my specialist subject because I'm writing a book about Baldwin and Churchill, the relationship between the two and issues which divided them. Above all rearmament and appeasement where Churchill blackened Baldwin's name, I think rather unfairly.

JS: What is the start point for that in your forthcoming book? What's the year in which that really gets going?

RO: With Baldwin becoming prime minister in 1923.

JS: Name a few people who have had a marked impact on your professional life as an investment manager and what you've gleaned from each of them?

RO: I think I think there have been three or four. Peter Stormonth Darling who was chairman of Mercury Asset Management then chairman of a family office that I managed was really a good friend and a mentor and a wonderful wise, calm, extremely nice very funny man. He was a good influence, particularly in in being calm in a crisis and his mantra was always do nothing which wasn't necessarily optimal as there's always something you can do which is better than doing nothing. But the point behind it is that, in a crisis, if you do something it is more likely to be damaging than doing nothing.

Another man who was quite an influence was Charles Goode who was chairman of ANZ in Australia and whom I used to see a lot of because I was a director of the Mercury Australia subsidiary. I remember him telling me that he cancelled an investment committee meeting in late 2008 because he thought that, if they met, they were bound to take a decision and it'd be much better that they shouldn't take any decision.

Peter Cundill, the Canadian Value investor, was a bit older than me and had a very strong influence. He was a very brave man he suffered from a disease called Fragile X. Fragile X, so called, because it was so obscure that nobody knew what to do about it and from which he died. It was a neurological illness. He died in 2011 and he was very brave during his dying. But in his investment, he was also very brave. At the end of every year, he loved to travel to the couple of markets that had performed worst in the previous year. He was drawn to things which had gone very badly and it's an interesting thing about the Warren Buffett essay of 1984 in which Buffett picked seven super investors who deserve that name because thereafter after 1984 they continue to be super investors.

[Editor:https://www.grahamanddoddsville.net]

But one of the things he pointed out was that every single one of them had had a significant period of three to five years of severe underperformance. Had Peter retired in 1999 after 25 years of running a Global Value fund, he would have underperformed from inception. When he actually retired in 2006, he was one of the superstars because the next seven years after 1999 were perfect for his approach. So you might think that that first 25 years was it all wasted. It wasn't because it was only by experiencing what he experienced that he could get the portfolio in the position in 1999 when it would then surge over the next six years. And to do that he had to be - and this was his mantra – “patient, patient, patient”. And, as I say, very brave.

Finally, and of course, Warren Buffett, who is great influence as for every Value investor.

JS: Either when you were studying, or in your first decade of work, were there any world events that seemed pertinent to you at the time and have proved so even today?

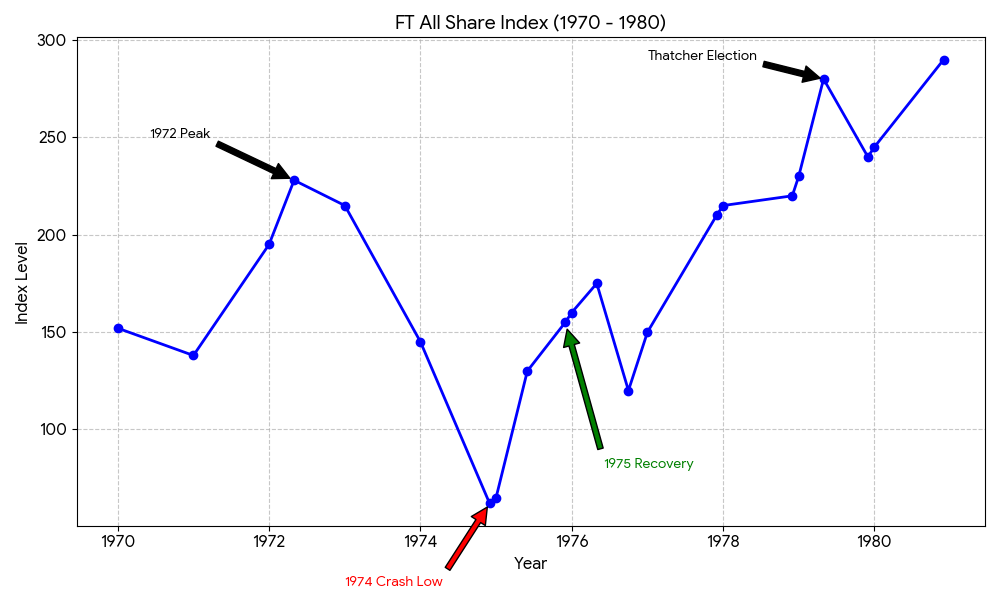

RO: The very first thing I was I was asked to do when I started work at Warburgs, was to write about the crash that had taken place the previous years when I was a student. The FT Ordinary Share Index (a precursor to the FTSE) had fallen by 55% in the 1974 and ’75 bear market. It then had a 136% rise in 1975 and a strong start to 1976. I wrote about this and so, in a way, that has set the scene for my interest in investment. What I'm most fascinated by is the is the mass psychology of markets. Of course I'm interested in businesses you can't do investment if you're not interested in businesses but it's the movement of markets that I find compelling. The episodes at the extreme are just fascinating. When you have excesses of gloom and you never quite know when you've reached the maximum point of gloom and when you have excesses of enthusiasm and you never quite know when you've reached the maximum point of enthusiasm. Those are the things that really fascinate me.

There's a lovely story about Peter Wilmot-Sitwell. He was the senior partner of the stockbrokers Rowe & Pitman. He was staying with the Queen Mother over Christmas and she thought he looked rather worried and she asked him what was concerning him and he said the stock market was in a terrible state. She replied “I'll pray for it”, which was prescient because I think it went up more than 50% in January.

Before that, the secondary banking crisis, the extremes of the banking crisis, depression in the UK, miners strike, the three-day week, doing revision by candle-light. Those days made a deep impression.

JS: Are there any popular theories, or schools of economics, that appear to you to be faulty or have not weathered well?

RO: Well, I think the really interesting thing is that none of them have weathered well. When I started work, Keynesianism was just in the middle of being dumped in favour of the Friedman free market view. Mrs. Thatcher, Ronald Reagan, the Laffer curve and so on. Friedman style economics then reigned supreme for the next 30 years until 2008. I think since 2008, it's been clear that totally free market economics is flawed.

Since then, what we’ve had in practice has been a blend of Keynesianism and Friedman. In QE, [Quantitative Easing] you have fiscal and monetary policy combined. There's no prevailing economic theory now that I think people are standing behind, and so it should be as any pure theory is probably bound to be flawed.

It does mean that people are rather at sea. Now the independence of central banks is being questioned. What Trump is doing is interesting in undermining the exorbitant privilege of the dollar, ever since April 8th last year because we've had policy volatility. Policies might turn out all right, but there's enormous volatility of policy and that idea of US exceptionalism has been undermined. All the old alliances are disappearing. The alliance between the US and Europe is fractured and that creates the opportunity for others to form alliances.

The geopolitical tectonic plates of the world are shifting dramatically. There used to be a nice cozy consensus among the central bankers who were largely independent. Now you have that independence questioned and also the consensus being questioned. Principally through the US President interfering and being so unpleasant to the current Fed chairman, he's ensuring that the next Fed chairman will play to his tune.

JS: If you were given the task of rebuilding economics as a study area from scratch and everybody currently doing economics today was discharged. What would be the foundation stone, you would build on?

RO: Well, first of all, I'm not an economist. I did PPE for one term and I sat down with David Lipsey’s enormous yellow book and thought I can’t face this after 100 pages and rang up [college admissions] and switched to history.

I don’t think it’s necessary for the Bank of England to have so many economists and for the public sector to employ them in practically every ministerial department. What is the point of them producing projections about this and that? Why not rely on investment bank economists instead?

JS: Can you name one or two people who produce arresting thoughts on markets on investment, but are not as well-known as they should be?

RO: They're mostly pretty well known. Warren Buffett has always produced arresting thoughts. So did Charlie Munger. Howard Marks (Oaktree Capital Management) writes very well, particularly about risk, including upside risk. Chris Wood (Jeffries equity strategist) is very stimulating, as is Jeremy Grantham (co-founder of GMO).

JS: You serve, and have served, as an external member of several investment committees. What makes a good external member of an investment committee?

RO: First of all, being realistic about individual levels of knowledge. We never know much of what is going to happen. So all one can do is attach probabilities. Your question is easier to ask in the inverse which is what makes a bad investment committee member? Be very wary of extreme dogmatism. Extreme dogmatism is almost by definition always wrong because of the nature of markets. Universal bearishness is an inverse indicator.

I can think of mistakes that I've made. I'll give you three. One is at Oxford University, when we formed a new investment committee and a new management company for the Oxford Endowment. At the first meeting, we talked about the fixed income markets and every member of the committee was in favour of junking fixed income. This was in this was in 2007 and there was one exception who was not a member of the committee, that was the adviser from Cambridge Associates, we brushed him aside and I think we I think we sold all the Treasury government fixed income positions. That was totally wrong and, as there is a real danger in feeding conventional wisdom, with the crowd all being in favour of one direction. We should have hesitated and thought: look if we're all so sure about this we ought to ought to worry about it a bit more.

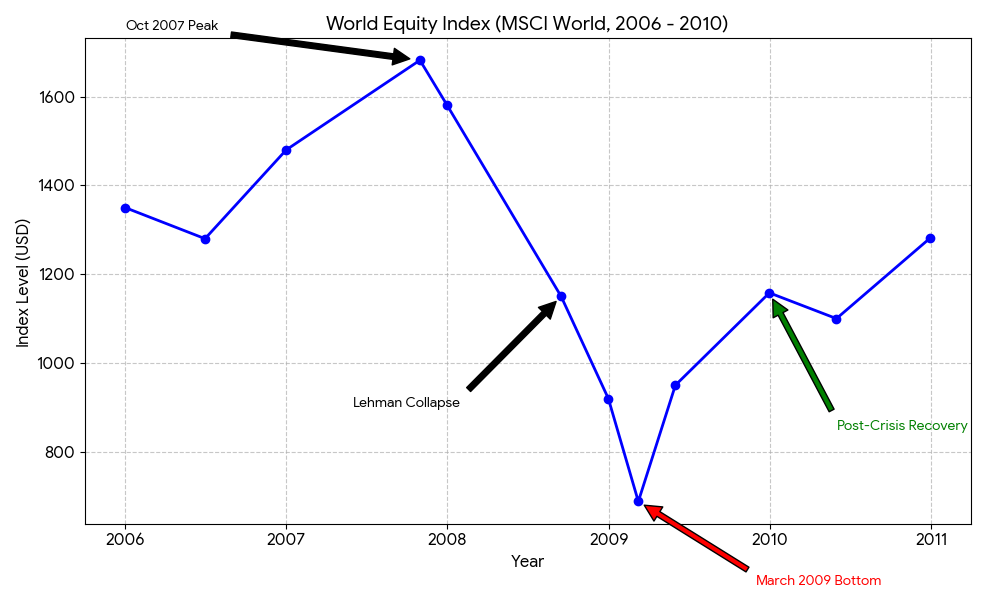

Another was in 2009 when there was a Technical analyst (chart reading) member of a family office investment committee that I was a member of. He became increasingly cautious, rightly, in 2007 and 2008. Then in March 2009 he said that we should sell all the equity positions. I took that as a sign.

JS: A counter sign? You mean a bullish signal?

RO: Yes. Particularly because, at the same time, I was a member of another investment committee for an institution where the outside manager said we have these allocation bands and we have a maximum level for equities. So we don't get too enthusiastic when we're enthusiastic. We don't get too gloomy when we're gloomy. But the position is now so strange, very unusual. We think you should drop below your minimum for equities. That date, March 2009, was the turning point, beginning of a great bull market. So, I think dogmatism is very dangerous. So a good investment committee member has to be not too dogmatic. They need to realise that all you are doing is playing around with probabilities. You may think something is strongly probable or not at all probable but you should never eliminate the possibility that something quite different happens.

JS: To bring it to today today, we have an enveloping war in the Middle East. What might interrupt the opening up of value and financial assets as the second order effects take place?

RO: What has happened so far is a major interruption. There were two themes over the last year, the first very much in favour of Value, especially outside the US. From April 8 2025, with American investors overloaded with US assets, they began to worry that they should look elsewhere and began to diversify internationally. They found companies which were languishing at very moderate valuations in markets outside the States and so that's been very good for Value investing in the last year, spectacularly good. This is a major interruption because suddenly people are worrying about where the safe haven is. Safe haven is quite a vague term. For some it means the US dollar as the major reserve currency. That is allied with the US as the major economy in the world. But now it means something quite specific: the place in the world least likely to be bombed, which happens to be again the US and then you have the US energy self-sufficiency. So, I think that's there’s been a major reversal in the last month. If it goes on, it won't be an interruption, it will be it will be a derailment.

RO: A recent Financial Times front page references “the spiralling Middle Eastern crisis” and I thought: is it spiralling? I'm not sure it is. I think it has spiralled.

JS: If the Gulf States run out of interceptors, that would be potentially a spiral.

RO: There are potential spirals, but it just may have finished spiralling. I'm attracted to some of the things which when this broke at the beginning of the month began to be worrying as they had done extremely well over the last year. I’m now reattracted to them at significantly lower prices.

JS: Your book on investment which is titled Simple but Not Easy was updated and reprinted in 2021. The financial world seems to get more complex and data heavy. Why is simplicity firstly so important and secondly potentially more elusive?

RO: The book was first printed in 2007 and then, as you say, updated in 2021. The point I would make is how ignorant one can be because it doesn't mention AI. I don't think those initials crop up anywhere. Things change remarkably quickly but I still think that with all the complexities that there are um I still think that investment is should be essentially simple in that it should concentrate on the essential issues and it's got more difficult to be simple because of the weight of information.

When I started work, you had a job getting the information. I started in the days of Telex. There weren't even fax machines. When I started in 1977, they were just appearing. To get the level of the what is now the Morgan Stanley Capital International World Index (MSCI) in order to plot by hand with a pencil on a chart the performance of the Mercury Global Fund, I had to ring up Madame Cissay at the Capital office in Geneva and ask her what the level of the world index was and I then put it on a chart and produced this pencil drawn chart. The world has changed dramatically in information terms, I think that makes it more important to keep it simple.

There's this plethora of information and the job is to sort through the information. One has to limit it rather than accumulate more and more. The risk is that you get stuck with analysis-paralysis. There's always more that you can find out. My point in the simple part of that title is to emphasise that one wants to concentrate on key issues and the rudiments of equity investing. I'm not talking about derivatives or structured products and so forth, but the rudiments of equity investing are basically quite straightforward.

The second part of the title is to point out that lay people tend to think that all professional asset managers should outperform the market. But of course they don't. It's axiomatic that they don't. That half of us will underperform. In fact, more than half because of costs. It's very difficult to be one of those who outperforms over the long run and impossible to be somebody who outperforms every year consistently.

Link to online bookseller [this one does not benefit Jeff & Lauren but they sell it as well]

Part II of the interview will be published later this week